Data confidentiality in financial auditing is a legal and ethical obligation that protects sensitive information processed by auditors throughout their mission. The auditor is subject to strict professional secrecy framed by articles 226-13 of the Penal Code and L.821-35 of the Commercial Code. The GDPR adds a formalized contractual layer, in particular via article 28 which imposes a subcontracting agreement (DPA) between the firm and its clients. The IIA and ISO 19011 professional standards complement this framework by making confidentiality a pillar of professional skepticism. In 2026, the integration of artificial intelligence into audit missions makes these requirements even more critical to master.

What are the legal obligations governing the confidentiality of financial audit data?

The professional secrecy of the financial auditor is based on two fundamental texts. Article 226-13 of the Penal Code criminalizes any disclosure of confidential information. Article L.821-35 of the Commercial Code reinforces this obligation for auditors.

The GDPR introduces a distinct and complementary contractual obligation. The absence of a DPA contract compliant with Article 28 is the most frequently identified non-compliance in audit firms in 2026. This contract must clarify who is the data controller and who is the subcontractor, a distinction often misunderstood in the field.

The distinction between controller and subcontractor weakens data protection when it is ignored. A firm that processes its client's data to carry out the audit acts as a subcontractor. This qualification imposes specific obligations: data security, notification of violations, assistance for the rights of the persons concerned.

Legal obligations also include limited exceptions. The TRACFIN declarations must remain strictly confidential, with data retention for five years and a ban on informing the client of the declaration. This legal obligation coexists with professional secrecy without contradicting it.

Professional secrecy is not absolute when it comes to supervisory authorities. During visit and seizure operations, a prior legal dialogue is recommended to organize a pre-sorting of confidential documents. This procedure protects both the auditor and his client.

The main non-compliance risks include:

- Absence of DPA: the firm processes personal data without a formalized subcontracting contract.

- Excessive retention: data is kept beyond legal periods without justification.

- Uncontrolled access: employees access data without formal authorization.

- Use of non-compliant tools: SaaS or AI tools are used without checking their GDPR compliance.

Pro tip: Before any engagement, check that your DPA explicitly covers sub-processors, including the audit software companies you use. An oversight at this level exposes the firm to direct liability.

How do the IIA and ISO 19011 standards strengthen data protection in auditing?

The IIA and ISO 19011 standards make confidentiality a fundamental principle, not a simple recommendation. Confidentiality is fundamental to enable frank and reliable sharing of sensitive information during the audit. Without confidentiality assurance, auditees withhold information, which directly compromises the quality of the auditor's work.

“Confidentiality is not a constraint imposed on the auditor. This is the condition that makes an honest and complete audit possible. » This principle, anchored in the IIA standards, reminds us that data protection is a lever of quality as much as an obligation.

The IIA standards structure privacy around three key principles:

1. Integrity: the auditor never discloses information obtained as part of his mission to unauthorized third parties, even after the end of the mission.

2. Professional conscience: the auditor systematically assesses the risks linked to the processing of sensitive data before using a tool or method.

3. Active confidentiality: the auditor takes concrete measures to protect data, in particular by limiting access and securing media.

The ISO 19011 standard complements this framework by recommending rigorous documentation of data flows during the audit. Each transfer of information must be traced and justified. This traceability protects the auditor in the event of a dispute and reinforces client confidence.

Integrating technology into audit engagements requires increased vigilance. The use of AI in auditing imposes pseudonymization of data, extensive audit rights on the systems used and transparency on processing metrics. These requirements are directly in line with the spirit of the IIA and ISO 19011 standards.

What are the practical challenges of confidentiality in external audit engagements?

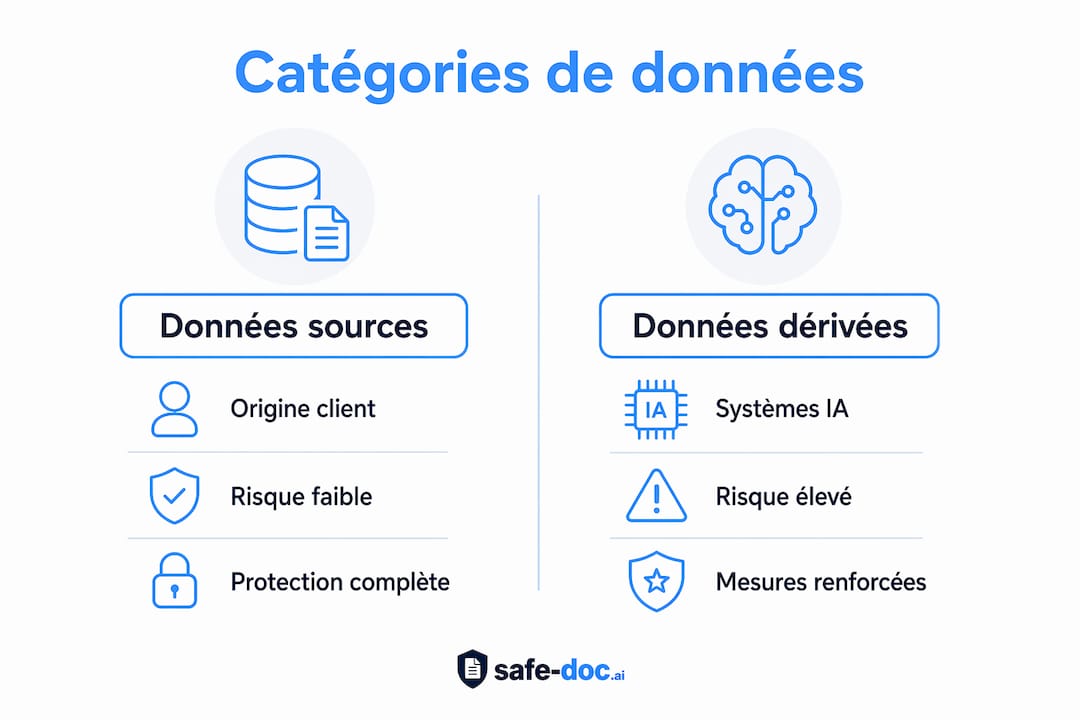

Auditors handle three categories of data with distinct legal statuses. The source data are those provided by the client: balance sheets, contracts, bank statements. Operational data is produced during the audit: working notes, analyses, working papers. The derived data are generated by the tools used: refined models, prompt logs, algorithm results.

The third category is the most risky and the least protected. Derived data produced by AI systems can become the property of the SaaS provider if the contracts do not explicitly claim them. A firm that uses an AI-based financial analysis tool can thus lose control of data with high intangible value.

| Data category | Origin | Main risk | Recommended protection |

|---|---|---|---|

| Source data | Customer | Unauthorized disclosure | Restricted access, encryption |

| Operational data | Listener | Excessive conservation | Formalized retention policy |

| Derived data | AI/SaaS tools | Supplier ownership | Explicit contractual clause |

The most common confidentiality violations in external auditing follow predictable patterns. An employee sends a client file to an unsecured online translation service. A team uses a generative AI tool without first pseudonymizing the data. An audit report is transmitted by unencrypted messaging. These situations expose the firm to GDPR sanctions and a loss of client confidence.

Shadow AI represents a particularly difficult risk to control. Employees use unapproved AI tools to save time, without measuring the consequences on financial information security. The firm remains responsible for these treatments even if it is not aware of them.

Pro Tip: Map the tools your audit teams use, including personal tools. An up-to-date processing log is the first line of defense against unintentional violations.

What mechanisms should be put in place to guarantee the protection of financial data?

Contractual formalization is the essential starting point. The DPA contract complies with article 28 GDPR must include provisions for confidentiality, security, breach notification, and assistance for individuals' rights. Very few firms implement it spontaneously, which makes it the main source of non-compliance identified during controls.

Clear segmentation of data into source, operational and derived data must be explicitly included in contracts. This clarification avoids disputes over the ownership of data of intangible value and protects the client's assets. A contract that does not mention derived data leaves a gray area that tool providers can exploit.

The organizational measures to be implemented cover several levels:

- Segmentation of access: each employee only accesses the data necessary for their mission, according to the principle of least privilege.

- Systematic pseudonymization: identifiable personal data (PIB) is pseudonymized before any processing by an external tool or AI.

- Access logging: each consultation or data transfer is recorded with the user's identity and timestamp.

- Retention policy: data is deleted according to a defined schedule at the end of the mission.

- Media encryption: workstations, USB keys and shared storage spaces are encrypted.

| Measurement | Tool or method | Related standard |

|---|---|---|

| Pseudonymization | Safe-doc, masking techniques | GDPR art. 4(5), AI Act |

| Encryption | AES-256, TLS 1.3 | ISO 27001 |

| Logging | SIEM, application logs | IIA, ISO 19011 |

| Training | E-learning modules, workshops | IIA Standard 1230 |

Team building is often underestimated. An auditor who understands why pseudonymization protects his firm and his client applies procedures with more rigor than an auditor who follows rules without understanding their logic. Quarterly awareness sessions, anchored in concrete examples of real violations, produce measurable results on behavior.

My view on confidentiality as an audit lever

Confidentiality is often presented as a regulatory constraint to be managed. My experience leads me to a different conclusion: it is a competitive advantage for firms that really master it.

A client who knows that their financial data is processed rigorously shares more information with their auditor. It signals areas of risk without fearing that this information will circulate. This frank sharing is exactly what professional skepticism requires to work. Confidentiality creates the conditions for a deeper and more useful audit.

The arrival of AI in audit missions changes the situation on one specific point: derived data. Most auditors are unaware that logs of their requests to an AI tool can become the property of the vendor. This is not a theoretical question. This is a contractual clause that I have seen go unnoticed in SaaS contracts signed by serious firms.

My most concrete advice: treat confidentiality as an audit process in its own right. Map data, formalize contracts, pseudonymize before dealing with AI. And make sure your DPA covers the tools your employees actually use, not just the ones you've officially approved.

— Jacques

Safe-doc: pseudonymization and compliance for financial auditors

Managing confidentiality in financial audits requires tools adapted to the constraints of GDPR and professional secrecy. Safe-doc offers a pseudonymization of sensitive data solution that allows audit teams to use AI tools like ChatGPT or Claude without exposing their clients' confidential information.

Safe-doc never stores processed documents and guarantees real-time processing. Personally identifiable data is masked before reaching the AI model and then returned in the final result. This architecture directly meets the requirements of Article 28 of the GDPR and the AI Act for high-risk systems. Audit firms that process sensitive financial data can thus maintain compliance without changing their working habits. For teams managing due diligence and data room operations, Safe-doc offers protection adapted to the volumes and sensitivity of the data at stake.

Frequently asked questions

What is confidentiality in an audit report?

Confidentiality in an audit report refers to the auditor's obligation not to disclose information obtained during the audit to unauthorized third parties. This obligation is governed by article 226-13 of the Penal Code and the IIA professional standards.

What are examples of confidentiality violations in auditing?

The most common violations include sending customer files to insecure online tools, using generative AI without prior pseudonymization, and transmitting reports via unencrypted email. These situations expose the firm to GDPR sanctions and a loss of client confidence.

What is confidentiality risk in financial auditing?

Audit confidentiality risk is the probability that sensitive information processed during the engagement will be disclosed, lost or used without authorization. This risk increases with the use of non-GDPR compliant SaaS and AI tools.

What confidentiality clauses should be included in an AI contract for auditing?

An AI contract for auditing should include clauses on ownership of derived data, prohibition of reuse of data to train the model, vendor's right to audit, and notification of violations. Explicit segmentation between source, operational and derived data is essential to avoid disputes.

How does pseudonymization protect financial data in audits?

Pseudonymization replaces personally identifiable data with fictitious identifiers before any external processing. It reduces the risk of a breach by rendering data unusable without the matching key, while allowing the auditor to work with AI tools without exposing their client's information.

Key points

Data confidentiality in financial auditing is based on three inseparable pillars: the legal framework (Penal Code, GDPR), professional standards (IIA, ISO 19011) and formalized technical measures including pseudonymization and encryption.

| Item | Details |

|---|---|

| Fundamental legal obligation | Professional secrecy (art. 226-13 and L.821-35) and the GDPR impose strict rules on all financial auditors. |

| DPA obligatory and often absent | The subcontracting contract compliant with article 28 GDPR is the most frequent non-compliance in firms in 2026. |

| Derived data at risk | The logs and models produced by the AI tools may become the property of the supplier without an explicit contractual clause. |

| Pseudonymization before any AI processing | Masking personal data before submitting it to an AI is the most effective technical measure to remain compliant. |

| Decisive team training | Privacy violations mostly come from untrained behavior, not technical failures. |