Financial statements are documents with a high density of personal data within the meaning of the General Data Protection Regulation. Pay slips, invoices, bank statements and tax returns all contain identifying information subject to GDPR obligations. For finance and data management professionals, ignoring this framework exposes the company to €20 million or 4% of annual global revenue. Compliance of personal data in GDPR financial statements is therefore not an option: it is a legal obligation active since 2018.

What personal data is included in the financial statements?

Financial statements contain much more than numbers. Each accounting document processes information that directly or indirectly identifies a natural person, which places them within the scope of the GDPR.

Here are the most common categories of personal data in financial documents:

- Identification data: surnames, first names, postal and electronic addresses of employees, customers and suppliers.

- Banking data: RIB, IBAN, account numbers, payment details.

- Tax data: SIREN numbers, tax numbers, VAT declarations, tax packages.

- Salary data: pay slips, remuneration amounts, social security contributions, sick leave.

- Contractual data: general conditions of sale, amounts invoiced, order history.

The distinction between sensitive and non-sensitive data remains important. Banking and tax data are not sensitive data in the strict sense of Article 9 of the GDPR, but they present a high risk in the event of a leak. Particular attention is therefore required.

An often overlooked point concerns liability for third party data. Financial professionals who work for B2B companies sometimes process the personal data of their own clients' end customers. This indirect responsibility considerably broadens the scope of compliance to be monitored.

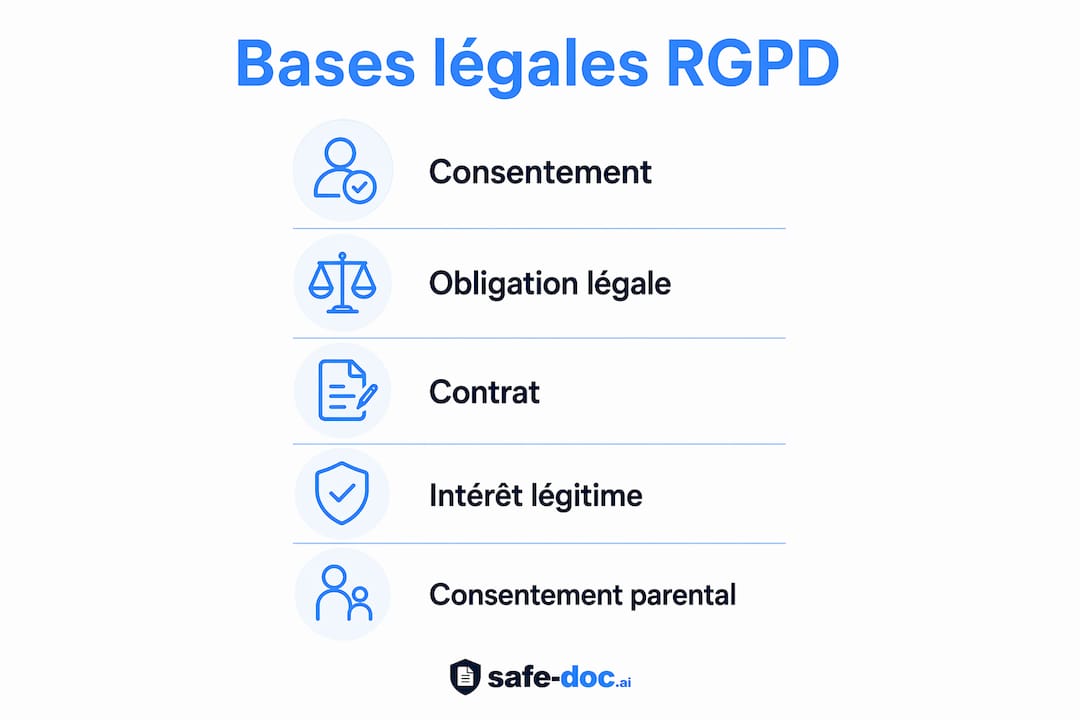

What are the legal bases for the processing of financial data?

The processing of personal data in financial statements is mainly based on two legal bases of the GDPR, without the need to obtain the consent of the persons concerned.

1. Legal obligation (article 6.1.c of the GDPR): The Commercial Code, the General Tax Code and social obligations require the keeping of certain accounting documents. The company has no choice: it must keep this data to comply with the law.

2. The execution of a contract (article 6.1.b of the GDPR): Invoicing, payment of salaries and management of suppliers require the processing of personal data. These processing operations are directly linked to the execution of contractual relationships.

3. Legitimate interest (article 6.1.f of the GDPR): Certain analytical or fraud prevention processing operations may be based on this basis, provided that the company's interest does not take precedence over the rights of the persons concerned.

These legal bases do not, however, exempt you from information obligations. The information notices must specify the purpose of the processing, the retention period and the rights of the individuals. This transparency is mandatory, even when consent is not required.

How to reconcile retention periods and the right to erasure?

Retention of financial data creates a real regulatory conflict. The right to erasure provided for by the GDPR is directly opposed to the legal retention periods imposed by accounting and tax law.

| Document Type | Legal retention period | Legal basis |

|---|---|---|

| Customer and supplier invoices | 10 years | Commercial Code |

| Pay slips | 5 years | Labor Code |

| Tax returns | 6 years | Book of tax procedures |

| Commercial contracts | 5 years | Civil Code |

The legal retention periods prevail over the right to erasure. This means that a person cannot demand the deletion of their data if their retention is required by law. This primacy is explicitly recognized by the GDPR in article 17.3.b.

Managing this conflict involves targeted purging of non-essential data, while retaining the minimum required transactional information. Concretely, an invoice must be kept for ten years, but superfluous contact data can be deleted as soon as the commercial relationship ends.

Pro Tip: Have a documented selective purge policy in place. Distinguish between data requiring mandatory retention and ancillary data, and schedule their automatic deletion at the legal deadline. This approach reduces risk exposure without violating accounting obligations.

What technical measures protect financial data?

The security of financial data is based on precise technical and organizational measures, imposed by Articles 25 and 32 of the GDPR. The Privacy by Design approach integrates these measures from the design of the systems, and not after the fact.

The essential technical measures to be put in place are as follows:

- Pseudonymization: replacement of personal identifiers with tokens or codes. The pseudonymization preserves traceability and auditability of financial statements while limiting data exposure. It differs from anonymization: the link with the individual remains technically reconstitutable, which allows internal audits.

- Encryption of data at rest and in transit: financial files stored on servers or exchanged by messaging must be encrypted. An intercepted unencrypted file constitutes a data breach under the GDPR.

- Access control: only employees who need access to financial data must have access to it. Fees must be reviewed regularly.

- Access logging: each consultation or modification of a financial statement must be traced to allow an audit in the event of an incident.

The risk of insecure AI tools deserves special attention. use of AI tools without a pseudonymization layer exposes major risks of unauthorized disclosure, particularly when manipulating financial statements. This phenomenon, known as Shadow AI, occurs when collaborators use consumer tools like ChatGPT to analyze documents containing unmasked personal data.

Pro Tip: Before using an AI tool to analyze a financial statement, always pseudonymize the document. Replace the names, RIB and tax numbers with neutral codes. Safe-doc applies this step automatically, without storing the original document.

The architectural security of your processing tools is as decisive as the measures applied to the data themselves. A tool that stores processed documents creates additional risk, even if the data is pseudonymized upstream.

How to prove GDPR compliance of financial statements?

GDPR compliance cannot be declared: it must be proven. The obligation of accountability imposed by Article 30 of the GDPR requires keeping a processing register documenting each personal data processing activity.

This register must contain, for each financial processing:

- The purpose of the processing (e.g.: payroll management, customer invoicing).

- The categories of data processed and the people concerned.

- The retention periods applied.

- Security measures put in place.

- Any subcontractors and transfers outside the EU.

Keeping a clear register is not only a legal obligation, but also the main tool for responding to CNIL controls and internal audits. A CNIL inspection without an up-to-date register exposes the company to immediate formal notice.

Audit preparation also involves documenting impact analyzes (IAPD) for high-risk processing, such as automated processing of large-scale salary data. This documentation demonstrates that the company assessed the risks before deploying its treatments.

Key points

GDPR compliance of financial statements is based on three inseparable pillars: documented legal bases, respected retention periods, and technical measures applied from the design of the systems.

| Item | Details |

|---|---|

| Legal bases without consent | Articles 6.1.b and 6.1.c of the GDPR cover the majority of financial processing. |

| Priority legal durations | Bills (10 years), payroll (5 years), tax (6 years) take precedence over the right to erasure. |

| Pseudonymization before anonymization | Pseudonymization preserves auditability while limiting data exposure. |

| Mandatory processing register | Article 30 of the GDPR requires each processing to be documented to prove compliance. |

| Shadow AI risk to be managed | Insecure AI tools expose financial data to uncontrolled leaks. |

What fifteen years of compliance taught me about financial statements

Most finance professionals approach GDPR as a do-once-and-forget-it project. This is the most costly mistake I see. Compliance is an ongoing process, not a fixed state. Systems evolve, subcontractors change, regulations are refined. What was compliant in 2022 may no longer be compliant in 2026.

What strikes me most is the systematic underestimation of indirect responsibility. An accounting firm that processes the financial statements of a B2B client often manipulates, without realizing it, the personal data of that client's end customers. Responsibility extends well beyond the visible perimeter. This reality requires vigilance that generic tools cannot ensure.

The real change in posture is to integrate data protection into financial tools from their design, and not to add a layer of compliance after deployment. Privacy by Design is not a theoretical concept: it is an architectural decision that is made when choosing software, data flows and access. Professionals who actually apply it pass their CNIL audits without stress. Others discover gaps under pressure.

— Jacques

Safe-doc to secure your financial data without changing your tools

Finance professionals who use AI tools to analyze financial statements face real risks if a layer of protection is not in place.

Safe-doc solves this problem by automatically pseudonymizing your sensitive documents before they reach an AI tool. Names, RIB, tax numbers and salary data are replaced by neutral tokens in real time. The original document is never stored. You continue to use ChatGPT or Claude as usual, but your data remains protected. The solution is designed to meet the requirements of Articles 25 and 32 of the GDPR, and integrates directly into existing workflows. Learn how pseudonymization and GDPR audit can apply to your financial statements, or review guide to GDPR pseudonymization to understand the technical differences between pseudonymization and anonymization.

Frequently asked questions

Do the financial statements contain personal data within the meaning of the GDPR?

Yes. Pay slips, invoices, RIB and tax declarations contain data allowing the identification of natural persons. The GDPR fully applies to these documents.

Can financial data be deleted at the request of a person?

No, if a legal obligation requires their retention. The legal durations (10 years for invoices, 5 years for payroll) take precedence over the right to erasure provided for in Article 17 of the GDPR.

What is the difference between pseudonymization and anonymization in financial statements?

Pseudonymization replaces identifiers with codes but retains the link with the individual, which allows audits. Anonymization permanently removes this link, making the document outside GDPR scope but unusable for internal controls.

Is a processing register required for financial data?

Yes. Article 30 of the GDPR requires any organization to keep a register documenting the purposes, durations and security measures for each processing operation, including accounting and financial processing operations.

What risks does the use of AI tools pose on non-pseudonymized financial statements?

Sending non-pseudonymized financial documents to consumer AI tools is a potential violation of GDPR. These tools can process and persist data in non-compliant environments, exposing the company to penalties and leaks of sensitive data.